LPLC continues to see claims involving land transfer duty (stamp duty) and other state property taxes.

What's on this page?

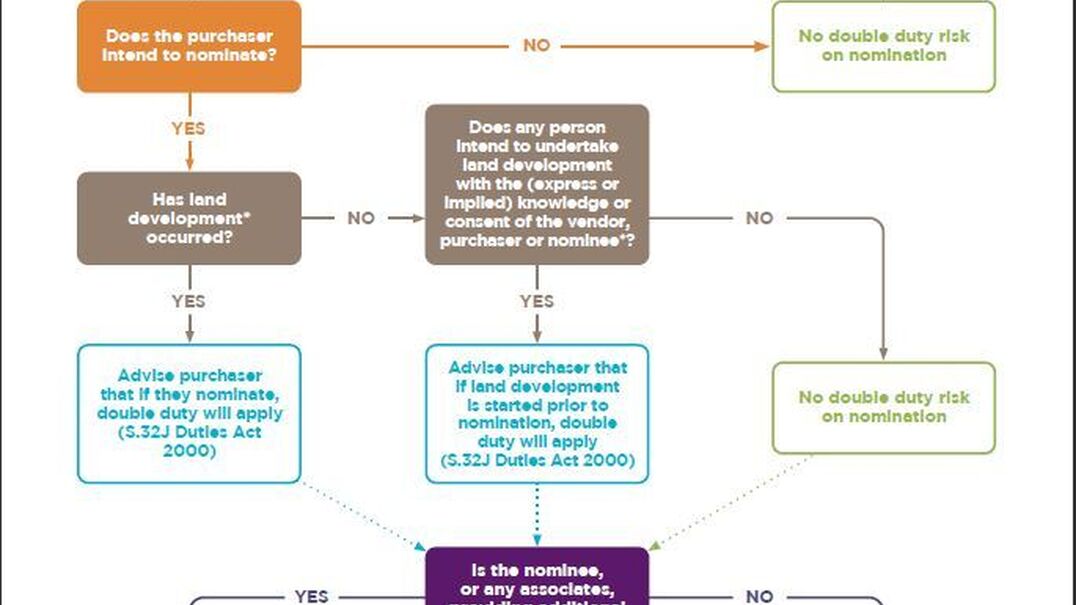

A common duty claim results from a purchaser nominating a

substitute purchaser or entity after they have applied for a building or

planning permit, resulting in a sub-sale that incurs a second assessment of

duty.

Section 32J and section 32C of the Duties Act 2000 (Vic) (the Act) set out the basis on which duty will be payable on transfers in certain circumstances involving nominations. While somewhat difficult to follow, it essentially says that double duty will be payable when a vendor agrees to transfer land to an original purchaser and then to a subsequent purchaser, often through nomination, in two circumstances:

- The subsequent purchaser pays or is liable to pay more consideration than the original purchaser.

- There is 'land development' after the initial contract data and the nomination date.

’Land development’ is defined broadly in section 3(l) of the Act and includes:

- preparing a plan of subdivision or taking steps to have it registered

- applying for or obtaining a planning permit

- applying for or obtaining a building permit or approval

- doing anything on the land for which a building permit or approval would be required

- requesting an amendment to a planning scheme that would affect the land

- developing or changing the land in any way which would increase its value.

The State Revenue Office provide guidance on the 'meaning of Land Development' in ruling DA-064v2 issued 31 October 2023.

Claims

Claims arise when the law firm fails to warn the client about their exposure to additional duty when they propose to nominate, or that conducting any ‘land development’ will result in an additional assessment of duty if they subsequently nominate.

Risk management

- Warn the client that there will be a second assessment of duty if there is ‘land development’ before nomination.

- Issue a specific advice letter raising the risk of double duty (and other nomination risks) and confirm the client's understanding before completing a nomination.

- Address these issues in a written general advice letter (often a pro forma or precedent letter) issued to every purchaser client at the commencement of your retainer.

Suggested wording

If you decide to nominate an additional or substitute purchaser there are several issues you need to consider including:

- additional duty may be payable if you undertake any land development before you nominate a new purchaser. Land development can include:

- applying for a planning or building permit

- preparing or registering a plan of subdivision

- requesting an amendment to a planning scheme

- doing any building works that would require a permit

- developing or changing the land in any way that would enhance its value.

- additional duty may be payable if the nominee gives you money and or some other consideration for the nomination

- you need to comply with any conditions in the contract of sale about nomination.

- a fee may be payable to the vendor for a nomination.

- we will need to prepare nomination document(s) which is outside the current scope of work we have given you.

- even if you nominate an alternate purchaser you (as the named purchaser in the contract) will remain liable for all obligations in the contract. If the nominated party defaults the vendor can pursue recovery from you. You are exposed to the risk that the nominated party defaults, causing you loss resulting from a claim by the vendor.

- Before proceeding with a nomination, we require your written acknowledgment of this advice and clear instructions to proceed.

Please contact us if you wish to discuss any aspect of this nomination advice.

This article was originally published on 2 December 2020, updated on 15 September 2021 and again on 17 October 2024.